Each other bucks-out refinance loans and you may household equity money should be offered privately inside the dollars

The fresh downside compared to that percentage option is you will start repaying interest towards complete loan amount instantly. Yet not, while the an earnings-away re-finance is actually substitution the 1st financial, may possibly not apply to your monthly premiums a lot (unless you alter the terms and conditions dramatically, for example supposed out-of a 30-12 months name in order to a great 15-12 months term). With a property collateral financing, you are and come up with payments towards your loan’s equilibrium and your current home loan repayments.

Which have a HELOC financing, you simply will not spend any desire until you withdraw money from the line of credit – and you will probably only pay appeal on the matter that you withdraw. Likewise, any number you pay-off goes back into the credit line. Such, for many who withdraw $5,000 regarding a good $10,one hundred thousand line of credit and you pay back $step three,000 once a couple months, payday loans Pemberwick CT online the personal line of credit might be $8,100000.

Things to Contemplate

In addition to the difference between interest levels and you may fee possibilities, there are numerous other factors to consider ahead of determining which type of mortgage best suits your needs, as well as this type of:

Extent You need

For folks who only need a small amount or if you you want availableness so you’re able to financing over time, good HELOC could be the best option because the you can pay only notice on what you withdraw and you will probably have access to the credit line for a while. If you want the money straight away however, just need a great touch, then a home collateral mortgage might be the better option, particularly when refinancing the home loan won’t trigger terms and conditions that will be a lot more beneficial than what you’ve got. The reason being if you get a funds-away refinance loan, you can easily will often have to cover settlement costs in advance (which can be pricey), whereas with property collateral financing, you can roll the newest settlement costs toward financing.

Each other home guarantee loans and cash-aside refinance funds is actually appropriate if you prefer large volumes out-of cash initial. It comes to be it worthy of substitution your existing mortgage and what you can manage to spend on a monthly basis – when you are to the a rigorous monthly budget, you do not be able to take on the extra repayments necessary for a property equity mortgage.

Number of Your Equity

One another dollars-away refinance finance and family guarantee funds require you to has actually about 20% security of your property. Thus each other sort of funds assists you to acquire up to 80 percent of your own residence’s value. However, which have an effective HELOC loan, you might use as much as 85 % of residence’s really worth depending on how creditworthy you are deemed to be.

Installment Period

Family security fund should be repaid inside the 5, ten, and 15-seasons episodes, whereas bucks-away refinance money may have terms doing 30 years (such as for instance a fundamental home loan). Normally, it’s a good idea to pay off property equity mortgage as easily as you’re able to just like the interest is high. Although not, this can be difficult according to your function since the you’re going to be settling your financial at the same time since you are purchasing away from your residence collateral mortgage, whereas your money-aside refinance mortgage merely changes your home loan.

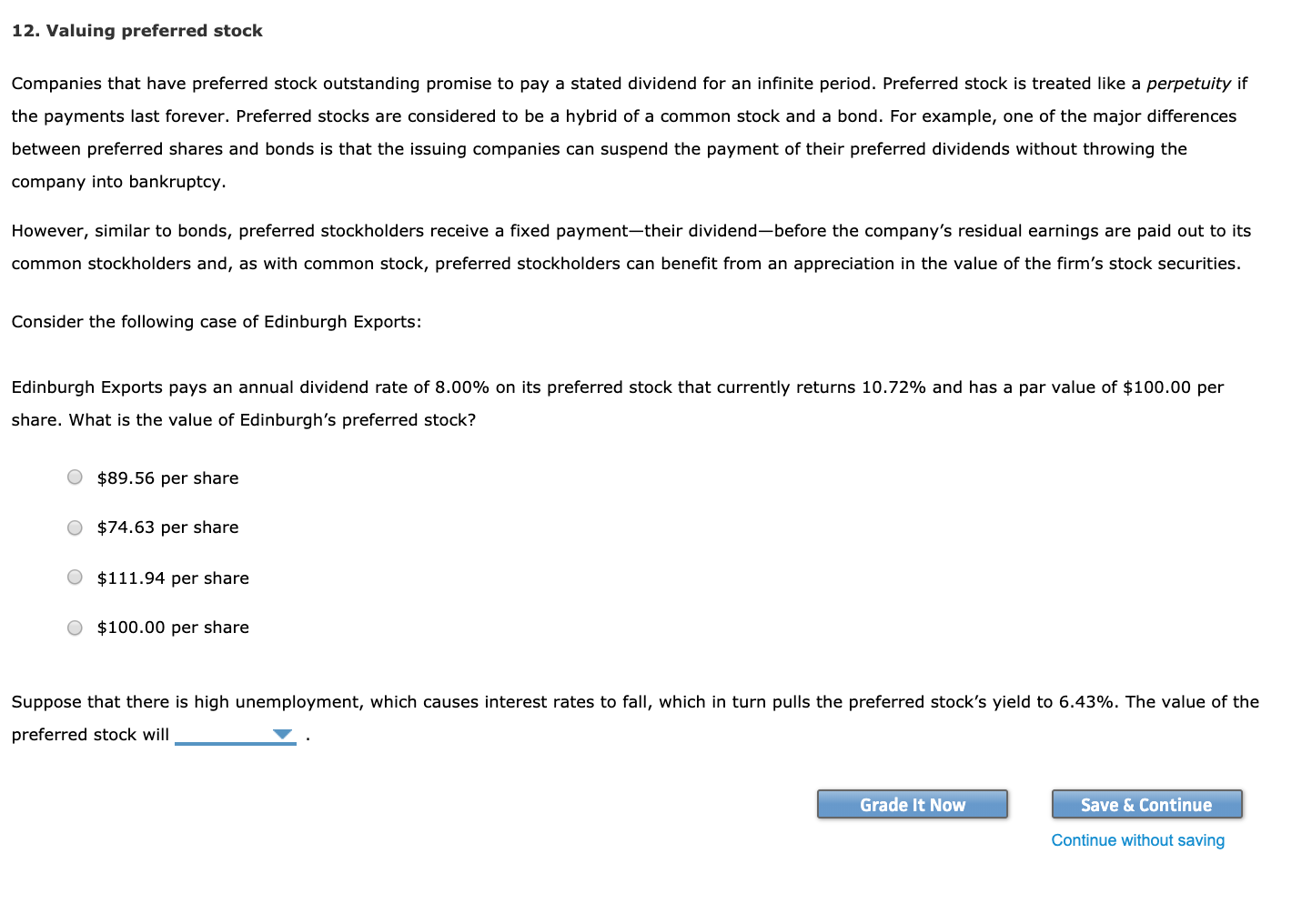

If you get a beneficial HELOC mortgage, you can purchase a great 20-year term that have a great ten-season draw period. It is possible to merely create repayments based on how much you withdraw regarding the personal line of credit.

Matter You are Prepared to Risk

Just because you may have a great amount of collateral of your property does not always mean you ought to borrow doing you could. You may be starting your property while the equity, after all, meaning that you are taking a danger. If everything is rigid economically, property guarantee loan would be a much bigger chance as it increases the total amount you only pay per month, whereas which have a money-away home mortgage refinance loan, this may potentially slow down the matter you only pay month-to-month with respect to the terms you choose.

Comments (0)